With the introduction of Kujira as an L1 blockchain on Cosmos, the team has launched their premier product — FIN. As an orderbook-style exchange, FIN facilitates the trading of assets on many different blockchains, with margin trading coming in the near future.

Within one week of launch, just under $1 million in volume has been traded through just two pairs: KUJI-axlUSDC and wETH-axlUSDC. Whilst this is impressive, we believe FIN has far more potential as a solution to inefficient DEX models that have become the standard in crypto for too long.

As you will see, orderbook-style exchanges have many advantages that allow them to be sustainable and long-lasting, rather than being propped up by inflationary incentives.

TLDR: Why Kujira’s FIN will thrive

- Improved trade execution for increased capital efficiency

- No reliance on inflationary incentives

- Scalable

- Cheap gas fees, as well as maker/taker fees.

- Future on/off-ramps for a better bridging experience.

Table of Contents

- How DEXs Work

- Disadvantages of AMMs

- Advantages / Disadvantages of Orderbooks

- Why FIN is scalable

- Lower Fees

- Superior Trade Execution

- User Interface

- Future Integrations

- Conclusion

How DEXs Work: A Natural Progression Of Decentralised Exchanges

When decentralised exchanges came to fruition in 2018, they quickly rose to prominence. By enabling Peer-to-Peer trading without intermediaries and maintaining anonymity, DEXs appeared to be a strong product/market fit.

However, a problem arose due to the fact that liquidity (capital available to trade) was often thin, producing large spreads (differences in price) between the lowest sell order and highest buy order. Typically, this isn’t a problem on a CEX since they garner huge amounts of liquidity and so can execute trades at smaller price intervals compared to a DEX with thin liquidity. As a solution, AMM (Automated Market Makers) were introduced.

How AMMs fixed liquidity issues

To solve the liquidity issue, AMMs use incentives to encourage all market participants to provide liquidity, not just those actively trading the asset. In the pursuit of capital efficiency, liquidity providers provide tokens to a liquidity pool which can be used to execute trades and are rewarded for doing so with inflationary rewards. This is commonly known as yield farming.

Disadvantages of AMMs

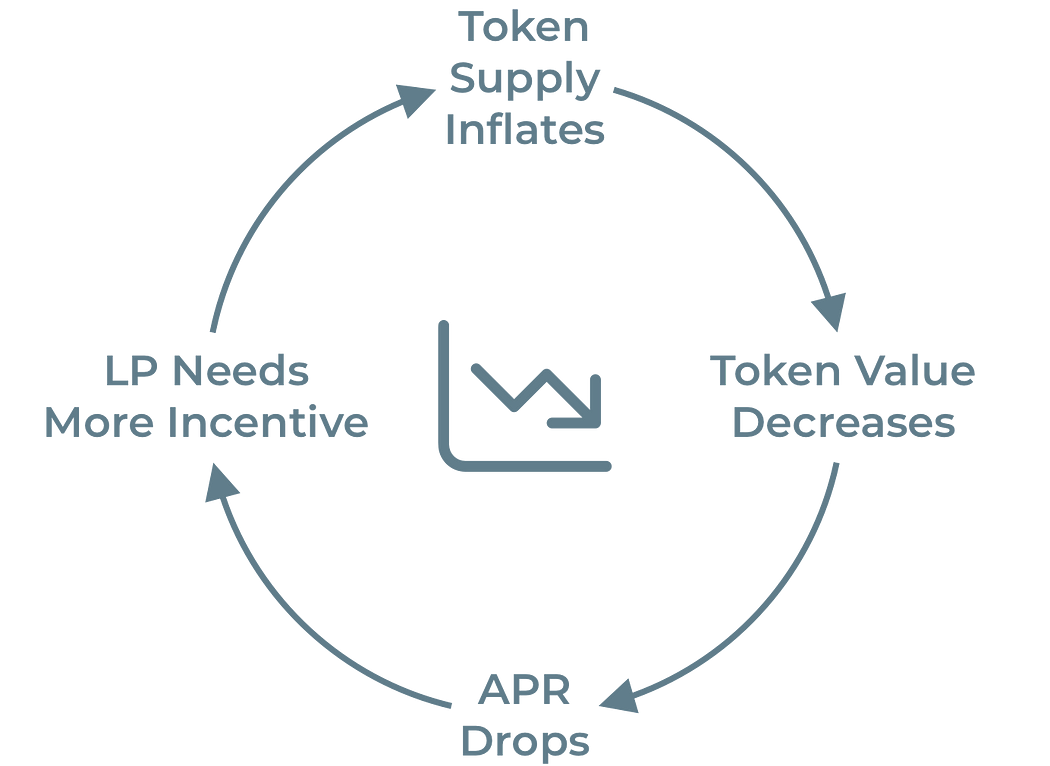

Inflationary rewards are unsustainable

Although this may improve the slippage by providing deeper liquidity, it becomes obvious that this model is unsustainable due to the use of inflationary rewards. It is a common misconception that most of the APR given for providing liquidity is in the form of “swap fees”.

In fact, the APR for swap fees alone is in most cases 0.5% within the Cosmos ecosystem, a stark contrast to the advertised APR in almost all examples.

Why AMMs Require Inflationary Rewards

Additionally, gas fees accrue in the underlying token, which is exposed to extreme volatility in the case of most cryptocurrency assets. Since LPs take on all the opportunity cost of an AMM by being exposed to this volatility (and so impermanent loss), they must be provided with a much higher APR to encourage them to take on this risk.

Tricky Future Of AMMs

We believe that inflationary incentives can be used as a short-term solution while the DEX creates other forms of revenue to drive profit. To use a similar example outside of crypto, Amazon ran at a loss for nearly 9 years before generating real revenue. During this time, they greatly increased their number of customers and produced many different streams of revenue, while choosing to run at a loss to advertise their product. Returning to AMMs, if there is no narrative to move from printing tokens to encourage LPs, to creating another revenue stream that creates value for the token, this system begins to fall flat.

As the token supply inflates, its value decreases without additional value, and the inflationary rewards begin to decrease in monetary value. As the APR for liquidity providers drops, the rewards may no longer worth the opportunity cost and they may pursue profit elsewhere, pulling liquidity.

Orderbooks

As the “solution” to low liquidity markets is a temporary fix rather than a long-term model, we believe the orderbook-style exchange is the best way forward. An orderbook does not require incentives to facilitate trade, simply market participants who wish to trade an asset by placing limit orders.

As FIN grows, liquidity will increase as traders migrate to a longer-lasting model that reduces their risk. In turn, this provides more buys and sells for a market maker to produce profit around the spread, causing them to tighten their bets around the central limit. Consequently, slippage is reduced as the spread between bids and asks is tightened to provide more profit for these market makers.

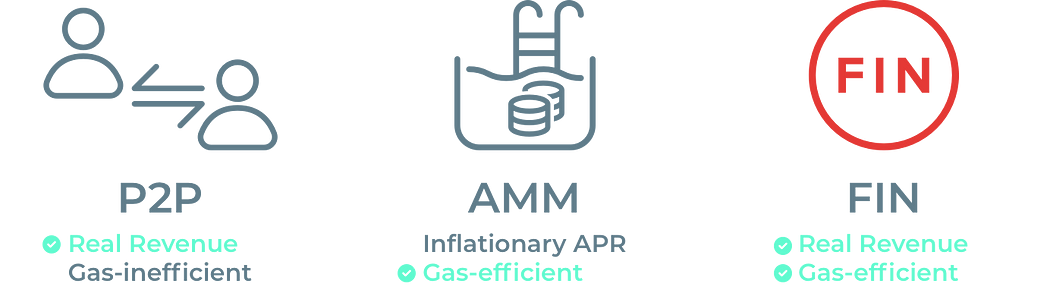

The orderbook model is tried and tested, with the NASDAQ being traded entirely using this system. The swap fees produced are real revenue that accrues to KUJI stakers and not liquidity providers. Recall that swap fees are accumulated in the underlying token, so KUJI stakers that secure the network are rewarded in a variety of assets in a non-inflationary manner.

Disadvantage Of Traditional Orderbooks

This section is quite complex, so I will provide some links to aid your understanding.

Since orderbooks must match each order individually, this becomes extremely computationally intensive. Inefficient matching algorithms lead to increased gas fees for every transaction; large CEXs overcome this via large banks of GPUs to match each order.

Why FIN Is Gas-Efficient And Scalable

Without giving away Hans’ Secret Sauce™, FIN has achieved a computational complexity of O(1). This means that the matching algorithm executes in the same amount of time, regardless of the number of orders.

Other orderbooks that use a traditional matching algorithm have achieved O(n), or at best O(log(n)). This indicates that the time taken to match orders increase linearly or to log(n) as more orders enter the market. Therefore, FIN is the best of both worlds – a gas-efficient orderbook that can scale easily.

But if users that are only trading the asset are providing liquidity and not rewarded, what is the incentive to trade and provide liquidity on FIN?

Fees

Fees on FIN are separated into two sections:

- Maker Fees — A fee paid if you place limit orders that are not immediately executed, and so “Make” liquidity in the books.

- Taker Fees — A fee paid if you place market orders and limit orders that are immediately executed. These “Take” liquidity from the books and so pay a larger fee.

Maker and taker fees are much lower on FIN relative to most AMMs. The standard fee for trading on an AMM is a flat 0.3%, over double what you pay on FIN.

Gas fees on Kujira are also extremely cheap, and users on FIN can pay in multiple different gas denominations. This is beneficial as when an asset increases in price, the gas will consequently cost more using this token; having the option to use a variety of assets allows customers to use the cheapest option at the time.

However, fees are often only an issue on Ethereum when the network is congested. Therefore in addition to low fees, FIN can guarantee trades will execute at better prices for the user.

Trade execution

Due to the mechanism in which orders are matched on orderbook-style exchanges, traders are guaranteed to execute orders at their specified price, or better. When you place a limit order, your trade will not be executed at a worse price, irrespective of the size of your trade.

Trade Execution On AMMs

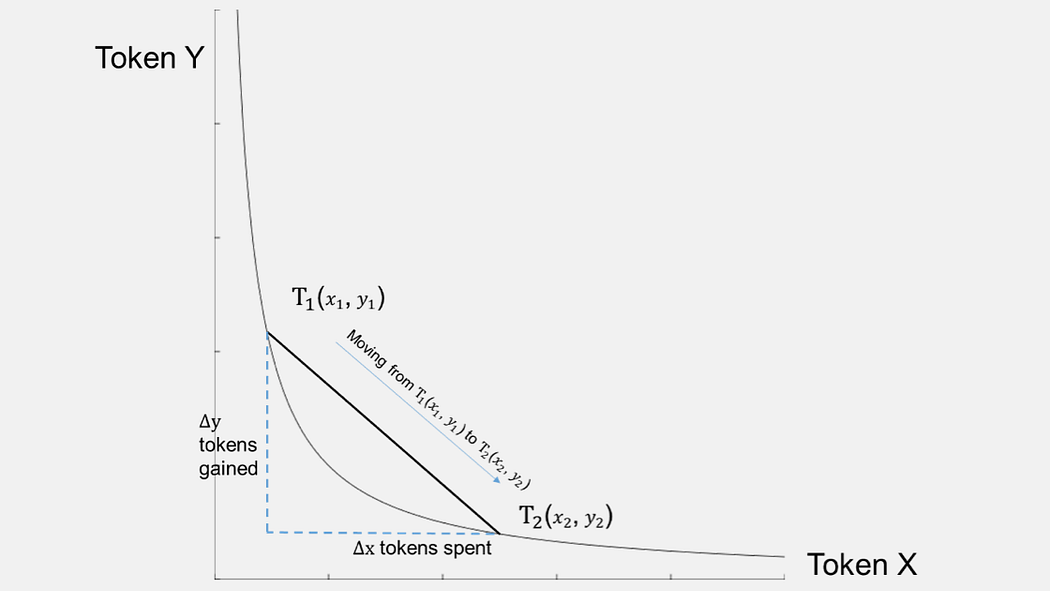

On an AMM, the price at which each trade is executed is calculated by the equation x * y = k.

Let’s go through this with an example: if a user wants to buy ETH (x) from the ETH-USDC pool, they will need to deposit USDC (y). This increases the amount of y in the pool and decreases the number of x tokens, as the user takes ETH (x) from the pool by providing USDC (y).

However, as x*y must always equal a constant, the price of ETH will increase as more is bought since less remains in the pool relative to USDC. Using this logic, when you place an order at the quoted price on an AMM, only the first token will trade at this price. This is because with each token purchased, the price per token will increase marginally such that you can only trade at the quoted price or worse.

Trade Execution On FIN

Since FIN is an orderbook-style DEX, trades are matched at the quoted price. This allows investors to “set-and-forget” limit orders, knowing that they will be executed with 0 slippage. The ability to set orders knowing the exact price where they will be traded is a huge quality of life upgrade and increases capital efficiency greatly.

Trade Execution On AMM/Orderbook “Hybrids”

As this is the topic of my next article, I will introduce this concept very briefly. With the emergence of Kujira recently, you may have seen a number of “orderbook DEXs” appear on your timeline.

Within these models, limit orders may be placed and are executed when the algorithmic price determined by the AMM is reached. However, orders are still traded via liquidity pools with inflationary incentives that are not sustainable. Furthermore, there are no order-to-order matching algorithms which introduce bias into who’s trades get executed (or not!).

Note — not all new orderbook DEXs work in this way.

Improving trade execution increases the capital efficiency of every transaction, guaranteeing you more tokens per trade. However, if you are a user with low initial capital this will benefit you less, so why is FIN still useful to you?

The User Interface

At Team Kujira, we pride ourselves on our User Interface’s aesthetics and hope you agree that Slangdog has smashed it again! The UI is intuitive and allows the trading of assets simply with minimal mouse clicks. Although, if the interface on FIN is unfamiliar to you, a guide can be found here that explains each component individually.

As an alternative, BLUE allows for simple market swaps for every asset traded on FIN. All orders are processed in the same way market orders are on FIN, we have just simplified the UI for you.

Bridging / fiat on-ramp (future integrations)

We understand that the bridging process is currently a barrier to entry for some users. A guide can be found here that explains all the possible routes currently available, however we have some exciting future partnerships that will make it easy to get money on FIN.

Integrations with Kado and LOCAL will allow direct fiat on-ramps into the Kujira ecosystem. Simply connect your bank details, deposit money into Kujira the Kujira network, and begin using our dApps.

Conclusion

FIN is a first-of-its-kind orderbook style DEX that incorporates the advantages of both AMMs and traditional orderbooks. By guaranteeing superior trade execution, low fees and a beautiful UI, FIN cements itself as a real competitor in the DEX space. Yet, the real beauty lies behind its simple matching algorithm that enables FIN to be scalable as liquidity and executed trades increase.

Additionally, with the passing of Proposal 15, Black Whale will begin building their Market-Maker-as-a-Service (MMaS). Market making helps to reduce the bid/ask spread and provides much deeper liquidity in our orderbooks. We look forward to integrating with new builders in the future, onboarding the next billion users to crypto. If you would like to build on Kujira, click here to find more details regarding our future Hackathon.

As a reminder, a full guide to bridging and trading on FIN can be found here.